Introduction

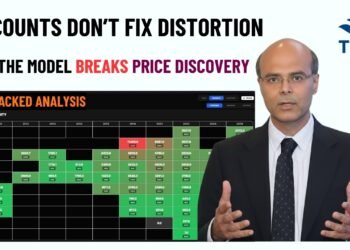

The table in the picture is a snapshot of the ratio of final auction price to the reserve price of spectrum across all circles and bands auctioned since 2010. In the picture different colors have been used to indicate spectrum of different bands. The length of the horizontal bar indicates the value of this ratio – the larger the length, higher is the ratio. The column on the sides with green shading are identical, and indicates the importance of the circles as per the AGR (Adjusted Gross Revenue) of the last quarter. Picture clearly tells the story that in most auctions, the final discovered price, has overshot the reserve price by multiple times. We all know that reserve price setting has always been an issue of serious discussion, both within the government, and between the stakeholders. Reserve price indicates the business potential of that circle in question, and lot of time and effort gets consumed in estimating this number. But, what is the point of all these efforts, if final discovered price is way off, and has little correlation with the reserve price set?

Was the Auction Design Faulty?

The huge difference between the final discovered price and the reserve price indicates that there was an issue with the auction design. If it wasn’t the case then the situation should have improved in successive auctions, as the normal practice is to link reserve price with the final discovered price of the immediate preceding auction, and time elapsed hasn’t been that long to cause a fundamental change in the market structure. Through the auction, government intended to maximize revenue, but ensuring the discovered price reflects the market realities was also government’s responsibility, more so when there weren’t any alternatives available for acquiring spectrum. This is extremely important, as optimal spend is bound to encourage operators to expand networks quickly in the remote areas as well, where profitability is a challenge. Excess spend on spectrum increases interest costs, and therefore discourages additional investments. Stringent roll out conditions and deferred payment clauses also does not help either, as roll out conditions are vague (subject to interpretations) and difficult to monitor, and deferred payments are counted as debt in the books and impacts valuation due to increased cash flows on account of regular principal/interest payments. Since the government is hard-pressed on funds for capital investments, encouraging private sector to make the necessary investments is all the more important, as much hyped “Digital India” needs access networks for these services to get delivered.

{kind=link}