The TRAI recently mandated telecom operators to introduce voice and SMS-only plans tailored for users who do not require data services, particularly those using feature phones. To assess the implications of this move, I previously analyzed the potential financial impact on operators if these plans were priced significantly lower to cater to this segment. Following the mandate, all operators have now introduced their respective plans. In this article, we will focus on evaluating the benefits these plans offer to users, particularly in terms of the cost of voice calls per minute, as calculated from the mobile usage trends (MOUs) reported by TRAI. We will also examine whether these new voice and SMS-only plans provide better value compared to existing data-inclusive plans, especially for users with minimal or no data needs.

Mobile Usage as Reported by TRAI in Their Latest Performance Report

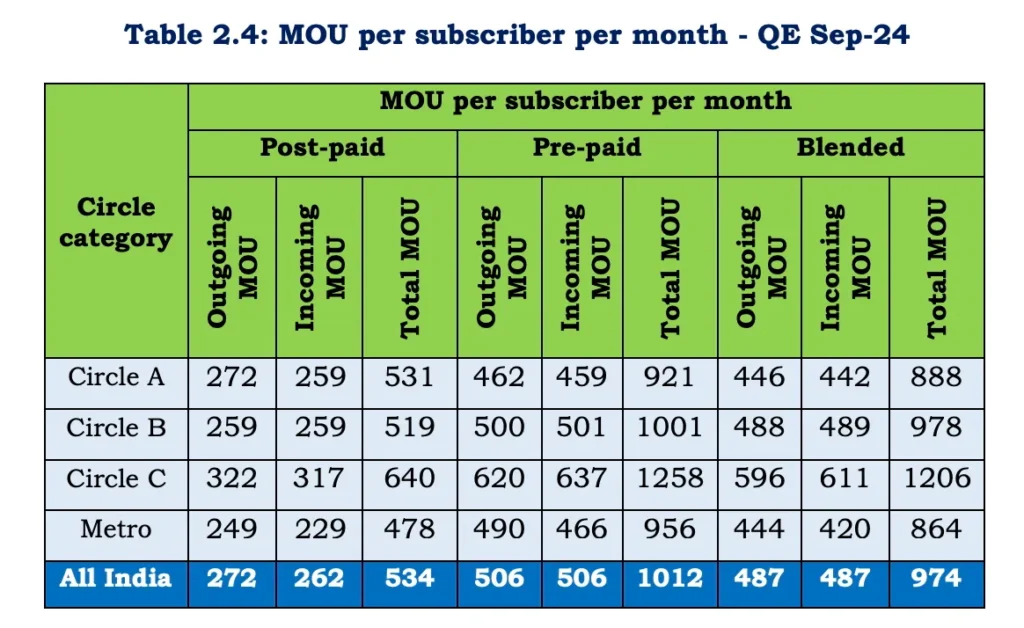

The table below is an extract from TRAI’s latest performance report, showcasing the Minutes of Usage (MOU) per month per subscriber for the Indian telecom sector across postpaid, prepaid, and blended segments.

Since all recently announced plans by telecom operators target the prepaid segment, we will use the All India prepaid MOU value of 1012 for calculating the cost per minute (in ₹) when comparing these plans. It is important to note that MOUs are influenced significantly by the availability of unlimited plans offered by operators, which tend to increase overall usage patterns as extracted out from the TRAI’s performance report for the blended MOU listed in the figure below.

The total MOU has witnessed significant growth, rising from 627 minutes per subscriber per month in Q2 FY19 to 974 minutes in Q2 FY25, highlighting a notable increase in overall mobile usage over the years.

Mobile Operators’ Voice Plans Compared to Their Nearest Data Plans

Using the All-India prepaid MOU of 1012 minutes per subscriber per month as a benchmark, let us compare the voice plans offered by mobile operators with their nearest data-inclusive plans that include minimal data capabilities. The comparison is summarized in the table below.

From the data:

- Airtel’s voice plans are 2 to 4 paise cheaper per minute compared to their nearest plans with limited data.

- RJIO’s voice plans are 1 paise cheaper than Airtel’s comparable plans and maintain similar pricing advantages over their own nearest data plans.

- VI’s voice plans also align closely with RJIO’s pricing trends, offering competitive per-minute costs while maintaining a slight advantage over their data-inclusive plans.

This analysis demonstrates that if current calling patterns persist, voice-only plans provide a marginally better cost advantage compared to plans with limited data, making them an attractive option for users who primarily focus on voice calls.

Conclusion

The introduction of voice and SMS-only plans by telecom operators, as mandated by TRAI, is a commendable effort to cater to feature phone users and those with minimal or no data needs. However, a closer look at the data suggests that the cost advantage of these plans, while present, is marginal—ranging from 1 to 4 paise per minute compared to their nearest data-inclusive counterparts. While this difference might appeal to a niche audience, it is not substantial enough to drive significant behavioral shifts.

Importantly, usage patterns must also be contextualized. If users switch to these voice-only plans, their mobile usage may align more closely with pre-2017 MOU trends, when lower data penetration resulted in heavier reliance on voice calls. For example, MOUs from that era (2017) provide a critical reference point, as they represent scenarios where data usage was less of a factor. This could result in a recalibration of per-minute costs, making voice-only plans potentially less competitive than they appear in the current high-MOU landscape influenced by unlimited plans.

Ultimately, this highlights a delicate balance for operators. Simply meeting regulatory mandates is not enough. To truly cater to the needs of low-data or voice-centric users, operators must design plans that not only reduce costs but also anticipate shifts in usage patterns as users revert to older behaviors. For consumers, the question remains: does the marginal cost saving justify the trade-off in flexibility?

Operators have an opportunity to rethink these plans, ensuring they are robust enough to sustain value for both low MOU-voice users and the overall telecom ecosystem. Without addressing these nuances—such as aligning with pre-2017 MOU usage patterns (400 MOU on average)—the plans fail to truly embody the spirit of the TRAI order. This risks the initiative being perceived as an attempt to circumvent the TRAI order rather than a genuine effort to provide meaningful and sustainable offerings for an evolving user base.

{kind=link}